|

|

|

VAT

|

|

|

Introduction

The VAT module is intended for the calculation of regular, corrective, supplementary and corrective additional VAT returns for the tax period for the continuous VAT payer, creation of inventories and recapitulation of documents and printing of these documents. A Summary Report is also created in the VAT module.

In order to achieve correct outputs, the correct setting of code lists and input of data into primary documents (invoices out - IO, advances in - AI, other receivables - OR, invoices in - II, advances out - AO, other liabilities - OZ, cash documents - CD, internal documents - ID, bank statements - BS).

In addition to the VAT module itself, this part of the documentation describes the correct setting of the code lists used in the primary documents and affecting the VAT return, and the methodologies for import and export, in which the procedures for issuing documents in K2 IS in connection with VAT.

|

|

|

Input of data into primary documents

|

|

|

Description of code lists

|

|

|

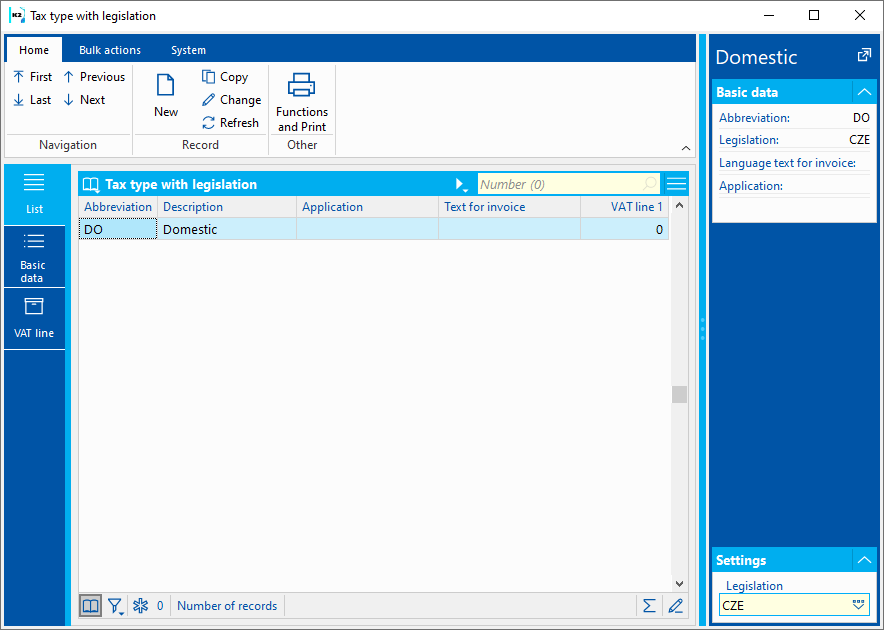

The code list contains types of VAT with regard to selected legislation, which characterize individual tax cases regardless of the specific amount of the VAT rate in a manner suitable for the classification / exclusion of the case to / from the individual areas of section C of the form for Value added tax return. The code list can be updated with the Import Tax Types script. In the record preview on the right, it is possible to select legislation - the records for the relevant legislation will be displayed.

Picture: Tax Type code list.

Meaning of check marks on the Basic data tab:

- For tax types for which self-assessment of VAT is created for the invoice received, the VAT self-assessment flag must be checked on the Basic data of the tax type tab.

- If the type of tax is stated in the VAT return only on the output, the Output only flag must also be checked (e.g. "EN" - Acquisition of article from the EU without the right to deduct).

- For types of taxes for which the self-assessment of VAT is performed on the provided advances, the flag Self-assessment of advances must be checked.

- For the type of taxes that are used for domestic performance in the regime of transfer of tax liability, the TTL regime flag must be checked.

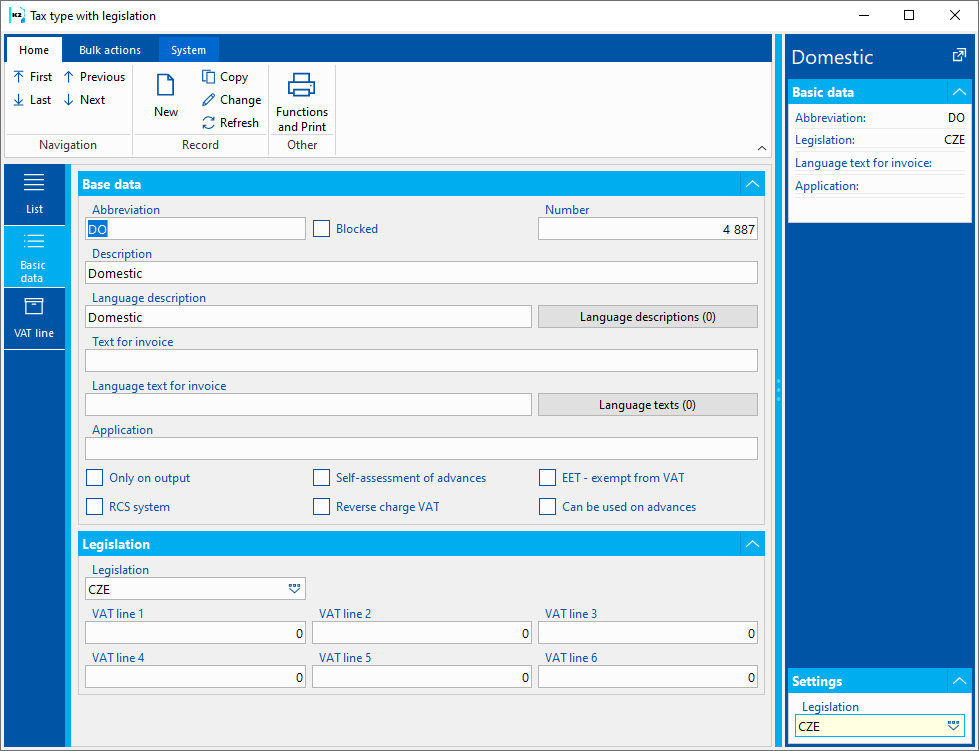

Picture: Tax Type code list - Basic Data

If the tax type has the VAT self-assessment flag checked, then if the VAT flag is checked in the tax recapitulation IO, II and in the items IA, OA, then when confirming these documents, a message about finding the tax type that is not to be used on VAT documents is displayed.

Note: The EET - bas_uns_vat check box is not related to the VAT return. It will be checked for types of taxes that are not intended for Czech legislation and are to be included in the Electronic Register of Sales in the element Total amount of transactions exempt from VAT, other transactions (e.g. customers of a Czech company pay by card at e-shops in Slovakia, Germany, etc.).

|

|

|

Process No: UCT005 |

Script ID number: FUCT050 |

File: ImportTaxType.PAS

|

Script description: Script for adding new types of taxes (in case of legislative changes to VAT). Loads new tax types from the TaxType.csv file, invoice texts from the TaxType_InvText.csv file, VAT line numbers TaxType_VatRow.csv. When launched, you will be asked "Do you want to import new tax types and update the description of all tax types?" After a positive answer, the tax types will be imported and updated. |

||

Address in the tree: [Accounting] [VAT] [Basic settings] |

||

Script parameters:

ImportInvoiceText - Yes Yes - tax types are updated, including the Invoice Text field; No - The text on the invoice will be added only for newly imported types of taxes. |

FileName - SupportFiles\Lang5\NewTax.csv Path and name of file |

Legislation = "CZE"

|

Interactive (boolean) = Yes

|

|

|

|

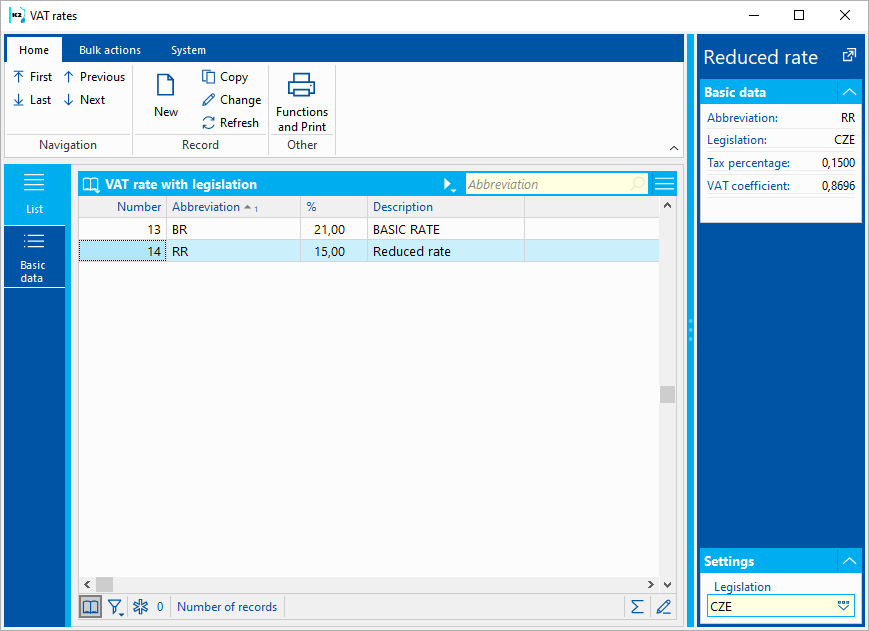

This code list contains individual tax rates (e.g. 21 %, 15 %). In the record preview on the right, it is possible to select legislation - the records for the relevant legislation will be displayed.

Picture: VAT rate code list with legislation

|

|

|

Types of taxes and tax rates on documents

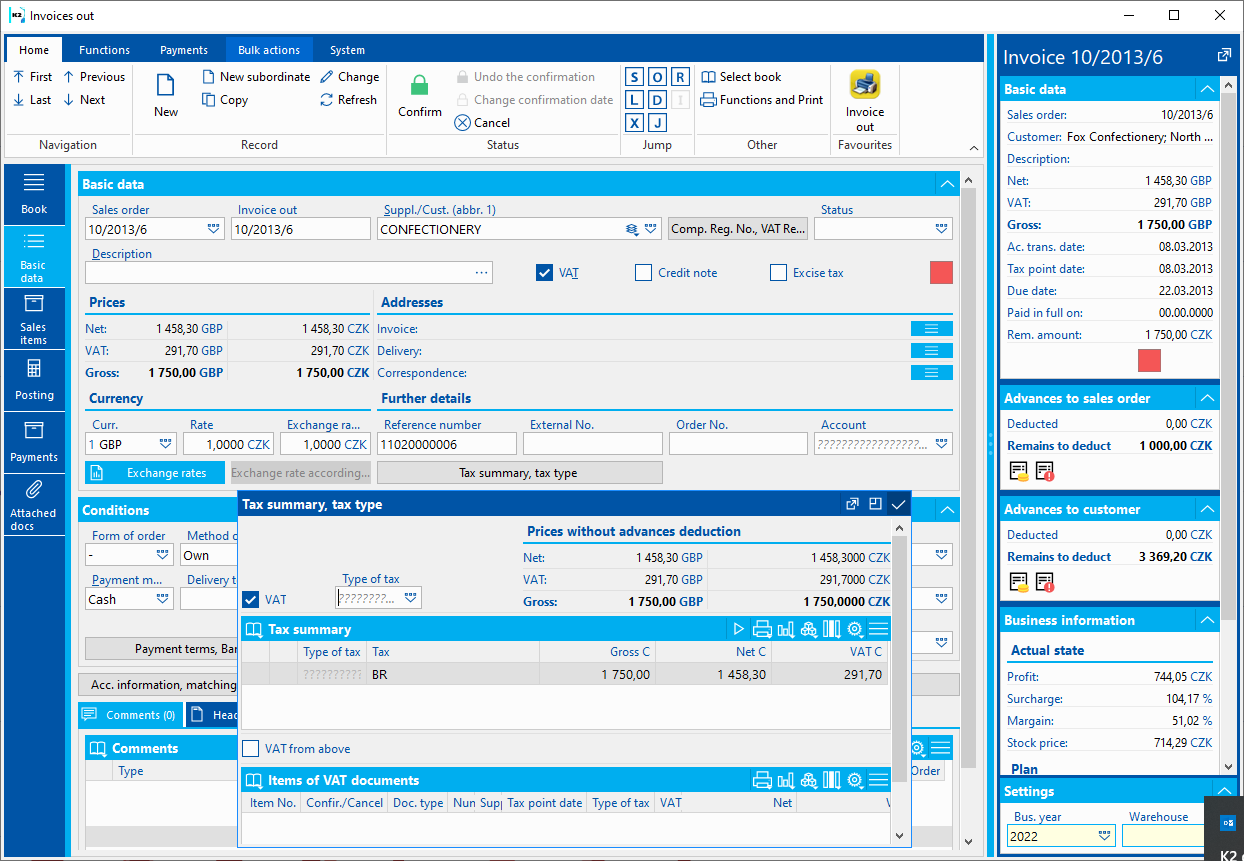

The type of tax and the VAT rate from the item of the document always apply to the VAT return on received and provided advances, other receivables and payables, cash and internal documents. The documents are subject to the Type of tax, the VAT rate and the Customs Tariff according to the legislation valid for the book. Documents cannot be copied between books from different legislations.

For bank statements (created in books in which VAT Documents is checked), the tax type (Tax Type field) and the tax rate (Tax field) can be entered in the document item.

The following rules apply to determine which type of tax each item of in and out invoices belongs to:

- If the document item does not have a Tax Type specified, then the tax type specified in the invoice header (Type field) applies to this document item.

- If a document item has a Tax Type specified, the tax type from the document header is ignored for that item.

The above mechanism ensures that each invoice item has a clearly identified type of tax and tax rate, which also allows it to be classified with respect to the individual lines of Section C of the value added tax return. Pressing Tax recapitulation button on Basic Data tab, you can find out what the price relations of the invoice are in terms of tax type and tax rate.

Picture: Grouping invoice prices by tax type and tax rate

|

|

|

Overview of types of taxes and their use in VAT returns from 1. 10 2021

Explanations:

"There must be a self-assessment document" means that an internal document will be created with the VAT quantified at the appropriate rate. A more detailed description of self-assessment documents can be found in the chapter Taxation of articles acquired from the EU.

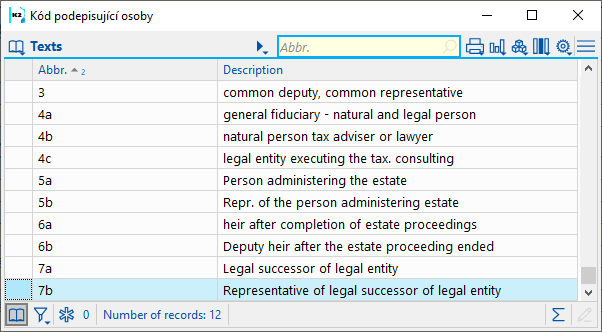

Abbr |

Description in K2 |

Detailed description |

|

|||

01 |

Import of articles |

Import of articles without customs |

There must be a self-assessment document |

|||

|

Application: |

It will be stated on lines 7/8 and 43/44 TR. |

||||

02 |

Import of articles with RE |

Import of articles without customs duty with reduction |

There must be a self-assessment document |

|

Application: |

It will be stated on lines 7/8 and 43/44 in the event of an obligation to reduce the right to deduct tax. |

|

03 |

Income - right to deduct - pv |

Deduction of tax on imports of articles |

|

|

Application: |

It will be stated on lines 43/44 DP. |

|

04 |

Income - right to deduct - ko |

Deduction of tax on imports of articles with deduction |

|

|

Application: |

It will be stated on lines 43/44 in the event of an obligation to reduce the right to deduct tax. |

|

05 |

Dispatch of articles to another Member State |

Dispatch of articles to EU |

|

|

Application: |

Sending articles to the EU in cases where the payer has exceeded the limit for sending articles. The subject of the tax is in the EU. It shall be entered on line 24 of TR. |

|

0P |

Transfer of tax liability of immovable property |

Transfer of tax liability regime - immovable property with a full right to deduct |

there must be document of self-assessment of VAT (for purchase) |

|

Application: |

It shall be used for the purchase of immovable property in Transfer of tax liability regime , it shall be stated on lines 10/11 and 43/44 with full deduction. It shall be used for the sale of immovable property in Transfer of tax liability regime , it shall be stated on line 25 TR. |

|

0K |

Transfer of tax liability of immovable property with DE |

Transfer of tax liability regime - immovable property with shortened right to deduct |

there must be document of self-assessment of VAT |

|

Application: |

It shall be used for the purchase of immovable property in Transfer of tax liability regime , it shall be stated on lines 10/11 and 43/44 with DE. |

|

0N |

Transfer of tax liability of immovable property without D |

Transfer of tax liability regime - immovable property without right to deduct |

there must be document of self-assessment of VAT |

|

Application: |

It shall be used for the purchase of immovable property in Transfer of tax liability regime , it shall be stated on lines 10/11. |

|

0M |

Transfer of tax liability of immovable property - asset |

Transfer of tax liability regime - immovable property with a full right to deduct - asset |

there must be document of self-assessment of VAT |

|

Application: |

It shall be used for the purchase of immovable property in Transfer of tax liability regime , it shall be stated on lines 10/11 11,/ 44 and 47 with full deduction. |

|

0A |

Transfer of tax liability of immovable property with DE asset. |

Transfer of tax liability regime - immovable property with a shortened right to deduct - asset |

there must be document of self-assessment of VAT |

|

Application: |

It shall be used for the purchase of immovable property in Transfer of tax liability regime , it shall be stated on lines 10/11 43,/44 and 47 with shortened right to deduction. |

|

0Q |

Transfer of tax liability of immovable property - forced sale |

Transfer of tax liability regime - immovable property forced sale with a full right to deduct |

there must be document of self-assessment of VAT (for purchase) |

|

Application: |

It shall apply to the purchase of immovable property sold by the debtor by a court decision in a compulsory sale procedure, in the regime of transfer of tax liability, it shall be stated on lines 10/11 and 43/44 with full deduction. It shall apply to the sale of immovable property sold by the debtor by a court decision in a compulsory sale procedure, in the regime of transfer of tax liability, it shall be stated on line 25 TR. |

|

0L |

Transfer of tax liability of immovable property FS with DE |

Transfer of tax liability regime - immovable property forced sale with a shortened right to deduct |

there must be document of self-assessment of VAT |

|

Application: |

It shall apply to the purchase of immovable property sold by the debtor by a court decision in a compulsory sale procedure, in the regime of transfer of tax liability, it shall be stated on lines 10/11 and 43/44 with DE. |

|

0O |

Transfer of tax liability of immovable property FS without D |

Transfer of tax liability regime - immovable property forced sale without a right to deduct |

there must be document of self-assessment of VAT |

|

Application: |

It shall apply to the purchase of immovable property sold by the debtor by a court decision in a compulsory sale procedure, in the regime of transfer of tax liability, it shall be stated on lines 10/11. |

|

0R |

Transfer of tax liability of immovable property FS - asset |

Transfer of tax liability regime - immovable property forced sale with a full right to deduct - asset |

there must be document of self-assessment of VAT |

|

Application: |

It shall apply to the purchase of immovable property sold by the debtor by a court decision in a compulsory sale procedure, in the regime of transfer of tax liability, it shall be stated on lines 10/11 11,/ 44 and 47 with full deduction. |

|

0B |

Transfer of tax liability of immovable property FS with DE asset. |

Transfer of tax liability regime - immovable property forced sale with a shortened right to deduct - asset |

there must be document of self-assessment of VAT |

|

Application: |

It shall apply to the purchase of immovable property sold by the debtor by a court decision in a compulsory sale procedure, in the regime of transfer of tax liability, it shall be stated on lines 10/11 43,/44 and 47 with shortened right to deduction. |

|

21 |

Transfer TL of telecommun. service |

Transfer of tax liability regime - wholesale telecommunication services with a full right to deduct |

there must be document of self-assessment of VAT (for purchase) |

|

Application: |

It shall be used for the purchase of telecommunication services (wholesale) in Transfer of tax liability regime , it shall be stated on line 10/11 and 43/44 with full deduction. It shall be used for the sale of telecommunication services (wholesale) in Transfer of tax liability regime , it shall be stated on line 25 TR. |

|

2P |

Transfer TL cereals |

Transfer of tax liability regime - cereals and industrial crops with a full right to deduct |

there must be document of self-assessment of VAT (for purchase) |

|

Application: |

It shall be used for the purchase of cereals and industrial crops in Transfer of tax liability regime , it shall be stated on line 10/11 and 43/44 with full deduction. It shall be used for the sale of cereals and industrial crops in Transfer of tax liability regime , it shall be stated on line 25 TR. |

|

2K |

Transfer TL cereals with DE |

Transfer of tax liability regime - cereals and industrial crops with a shortened right to deduct |

there must be document of self-assessment of VAT |

|

Application: |

It shall be used for the purchase of cereals and industrial crops in Transfer of tax liability regime , it shall be stated on line 10/11 and 43/44 with DE. |

|

2N |

Transfer TL cereals without D |

Transfer of tax liability regime - cereals and industrial crops without right to deduct |

there must be document of self-assessment of VAT |

|

Application: |

It shall be used for the purchase of cereals and industrial crops in Transfer of tax liability regime , it shall be stated on line 10/11 TL. |

|

3P |

Transfer TL metals |

Transfer of tax liability regime - metals with a full right to deduct |

there must be document of self-assessment of VAT (for purchase) |

|

Application: |

It shall be used for the purchase of metals in Transfer of tax liability regime , it shall be stated on lines 10/11 and 43/44 with full deduction. It shall be used for the sale of metals in Transfer of tax liability regime , it shall be stated on line 25 TR. |

|

3K |

Transfer TL metals with DE |

Transfer of tax liability regime - metals with shortened right to deduct |

there must be document of self-assessment of VAT |

|

Application: |

It shall be used for the purchase of metals in Transfer of tax liability regime , it shall be stated on lines 10/11 and 43/44 with DE. |

|

3N |

Transfer TL cereals without D |

Transfer of tax liability regime - metals without right to deduct |

there must be document of self-assessment of VAT |

|

Application: |

It shall be used for the purchase of metals in Transfer of tax liability regime , it shall be stated on lines 10/11 TL. |

|

41 |

Domestic - asset |

Domestic compensation with the right to deduction |

|

|

Application: |

Domestic compensation with the right to deduct incl. provided payments stated on line 40/41 and also on l. 47 TR. |

|

42 |

Domestic RC with DE - asset |

Domestic RC with deduction |

|

|

Application: |

It shall apply to compensation received in the Czech Republic with the obligation to reduce the right to deduct tax and when providing payment for such compensation. It will be stated on lines 40/41 and 47 TR. |

|

43 |

Import of artic. admin. CO - asse. |

Import of articles, where administrator is CO |

There must be a self-assessment document |

|

Application: |

It shall be stated for the compensation on l. 7/8, 42 and at the same time on line 47 TR. |

|

44 |

Import of art. CO administration - asse. |

Import of articles, where administrator is Custom office |

|

|

Application: |

It will be stated on lines 42 and at the same time on l. 47 TR. |

|

45 |

Import of artic. admin. CO with DE - asse. |

Import of articles, where administrator is Custom office with deduction |

There must be a self-assessment document |

|

Application: |

It shall be stated for the compensation on l. 7/8, 42 and at the same time on line 47 TR. |

|

46 |

Imp. Of art. adm. CO - asse. with DE |

Import of articles, where administrator is Custom office with deduction |

|

|

Application: |

It will be stated on lines 42 and at the same time on l. 47 TR. |

|

47 |

Provision of ser. to asse. from the EU |

Receipt of a service from a taxable person in the EU |

There must be a self-assessment document |

|

Application: |

It will be stated on lines 5/6, 43/42 and at the same time on l. 47 |

|

48 |

Provision of ser. to asse. from the EU with DE |

Receipt of a service from a taxable person in the EU with deduction |

There must be a self-assessment document |

|

Application: |

It will be stated on lines 5/6, 43/42 and at the same time on l. 47 TR. |

|

49 |

Import of articles - asset |

Import of articles |

There must be a self-assessment document |

|

Application: |

It will be stated on lines 7/8, 43/42 and at the same time on l. 47 TR. |

|

4A |

Import of articles DE- asset |

Import of articles with DE |

There must be a self-assessment document |

|

Application: |

It will be stated on lines 7/8 and 43/44 and at the same time on l. 47 TR. |

|

4B |

Provision of ser. to asse. OT |

Other taxable compensation |

There must be a self-assessment document |

|

Application: |

It will be stated on lines 12/13, 43/42 and at the same time on line 47 TR. |

|

4C |

Provision of ser. to asse. OT with DE |

Other taxable compensation with deduction |

There must be a self-assessment document |

|

Application: |

It will be stated on lines 12/13, 43/42 and at the same time on line 47 TR. |

|

4P |

Transfer Tax liability mobile phones |

Transfer of tax liability regime - mobile phones with a full right to deduct |

there must be document of self-assessment of VAT (for purchase) |

|

Application: |

It shall be used for the purchase of mobile phones in Transfer of tax liability regime , it shall be stated on lines 10/11 and 43/44 with full deduction. It shall be used for the sale of mobile phones in Transfer of tax liability regime , it shall be stated on line 25 TR. |

|

4K |

Transfer Tax liability mobile phones with DE |

Transfer of tax liability regime - mobile phones with shortened right to deduct |

there must be document of self-assessment of VAT |

|

Application: |

It shall be used for the purchase of mobile phones in Transfer of tax liability regime , it shall be stated on lines 10/11 and 43/44 with DE. |

|

4N |

Transfer Tax liability mobile phones without DE |

Transfer of tax liability regime - mobile phones without right to deduct |

there must be document of self-assessment of VAT |

|

Application: |

It shall be used for the purchase of mobile phones in Transfer of tax liability regime , it shall be stated on lines 10/11 TL. |

|

4V |

Domestic - asset, CR B2 |

Domestic compensation with the right to deduction, CR always B2 |

|

|

Application: |

Domestic compensation with the right to deduct stated on line 40/41 and also on l. 47 TR. It is always displayed in section B2 in the control report. |

|

4W |

Domestic with DE- asset, CR B2 |

Domestic RC with deduction, CR always B2 |

|

|

Application: |

It shall apply to compensation received in the Czech Republic with the obligation to reduce the right to deduct tax. It will be stated on lines 40/41 and 47 TR. It is always displayed in section B2 in the control report. |

|

50 |

Provid. ser. outside the country |

Provid. services outside the country to a person registered in the EU - IO, AI, OT |

|

|

Application: |

The value of the compensation (or the value of the consideration received preceding the supply) in the case of the supply of services outside the country to a taxable person in another Member State shall be provided. It shall be entered on line 21 of TR. |

|

51 |

Other compensation with he right to deduct tax |

Other compensation with he right to deduct tax |

|

|

Application: |

It shall apply to other exempt compensation with the right to deduct and payments received. It is included in line 26. |

|

52 |

ND compensation NI in the coef. |

Non - domestic compensation not included in the coefficient |

|

|

Application: |

It shall apply to amounts for performed compensations which are not included in the calculation of the coefficient pursuant to Section 76, Paragraph 4 upon receipt of payment for such compensation. It will be indicated on line 51 with the right to deduct and on line 1/2 TR. |

|

55 |

ND compensation NI in the coef., CR always A4 |

Non - domestic compensation not included in the Coefficient, CR always A4 |

|

|

Application: |

It shall apply to amounts for performed compensations which are not included in the calculation of the coefficient pursuant to Section 76, Paragraph 4 upon receipt of payment for such compensation. It will be indicated on line 51 with the right to deduct and on line 1/2 TR. It is always displayed in section A4 in the control report. |

|

53 |

Exempt compensation without the right to deduct |

Exempt compensation without right to deduct |

|

|

Application: |

It shall apply to amounts for exempt compensation without right to to deduct. It will be indicated on line 50 TR. |

|

54 |

Compensation without the right to deduct DO NOT include in the coefficient |

Compensation not included to coefficient |

|

|

Application: |

It shall apply to amounts for exempt compensation without right to Deduct, included on l. 50 TR and on l. 51 TR without right to deduct. |

|

5P |

Transfer TR integrated circuits |

Transfer of tax liability regime - integrated circuits with a full right to deduct |

there must be document of self-assessment of VAT (for purchase) |

|

Application: |

It shall be used for the purchase of integrated circuits in Transfer of tax liability regime , it shall be stated on line 10/11 and 43/44 with full deduction. It shall be used for the sale of integrated circuits in Transfer of tax liability regime , it shall be stated on line 25 TR. |

|

5K |

Transfer TR integrated circuits with DE |

Transfer of tax liability regime - integrated circuits with shortened right to deduct |

there must be document of self-assessment of VAT |

|

Application: |

It shall be used for the purchase of integrated circuits in Transfer of tax liability regime , it shall be stated on line 10/11 and 43/44 with DE. |

|

5N |

Transfer TR integrated circuits without DE |

Transfer of tax liability regime - integrated circuits without right to deduct |

there must be document of self-assessment of VAT |

|

Application: |

It shall be used for the purchase of integrated circuits in Transfer of tax liability regime , it shall be stated on line 10/11 TL. |

|

5I |

Provid. ser. outside the country |

Delivery of articles incl. installation or assembly into the EU - IO, AI, PO |

|

|

Application: |

The value of the compensation (or the value of the consideration received preceding the supply) in the case of the supply of services outside the country to a taxable person in another Member State shall be provided. It shall be entered on line 21 of TR. |

|

5Z |

Provid. ser. outside the country |

Provid. services outside the country to a person registered in the EU - IO, AI, OT |

|

|

Application: |

The value of the compensation (or the value of the consideration received preceding the supply) in the case of the supply of services outside the country to a taxable person in another Member State shall be provided. It shall be entered on line 21 of TR. |

|

6P |

Transfer TR automated data processing equipment |

Transfer of tax liability regime - portable devices for automated processing with a full right to deduct |

there must be document of self-assessment of VAT (for purchase) |

|

Application: |

It shall be used for the purchase of portable devices for automated processing in Transfer of tax liability regime , it shall be stated on line 10/11 and 43/44 with full deduction. It shall be used for the sale of portable devices for automated processing in Transfer of tax liability regime , it shall be stated on line 25 TR. |

|

6K |

Transfer TR automated data processing equipment with DE |

Transfer of tax liability regime - portable devices for automated processing with shortened right to deduct |

there must be document of self-assessment of VAT |

|

Application: |

It shall be used for the purchase of portable devices for automated processing in Transfer of tax liability regime , it shall be stated on line 10/11 and 43/44 with DE. |

|

6N |

Transfer TR automated data processing equipment without DE |

Transfer of tax liability regime - portable devices for automated processing without right to deduct |

there must be document of self-assessment of VAT |

|

Application: |

It shall be used for the purchase of portable devices for automated processing in Transfer of tax liability regime , it shall be stated on line 10/11 TL. |

|

6M |

Transfer TR automated data processing equipment asse. |

Transfer of tax liability regime - portable devices for automated processing with a full right to deduct - assets |

there must be document of self-assessment of VAT |

|

Application: |

It shall be used for the purchase of portable devices for automated processing in Transfer of tax liability regime , it shall be stated on line 10/11 11,/ 44 and 47 with full deduction. |

|

6O |

Transfer TR automated data processing equipment with DEasse |

Transfer of tax liability regime - portable devices for automated processing with shortened right to deduct - assets |

there must be document of self-assessment of VAT |

|

Application: |

It shall be used for the purchase of portable devices for automated processing in Transfer of tax liability regime , it shall be stated on line 10/11 43,/44 and 47 with shortened right to deduction. |

|

7P |

Transfer TR video game console |

Transfer of tax liability regime - video game console with a full right to deduct |

there must be document of self-assessment of VAT (for purchase) |

|

Application: |

It shall be used for the purchase of video game console in Transfer of tax liability regime , it shall be stated on line 10/11 and 43/44 with full deduction. It shall be used for the sale of video game console in Transfer of tax liability regime , it shall be stated on line 25 TR. |

|

7K |

Transfer TR video game console with DE |

Transfer of tax liability regime - video game console with shortened right to deduct |

there must be document of self-assessment of VAT |

|

Application: |

It shall be used for the purchase of video game console in Transfer of tax liability regime , it shall be stated on line 10/11 and 43/44 with DE. |

|

7N |

Transfer TR video game console without DE |

Transfer of tax liability regime - video game console without right to deduct |

there must be document of self-assessment of VAT |

|

Application: |

It shall be used for the purchase of video game console in Transfer of tax liability regime , it shall be stated on line 10/11 TL. |

|

8P |

Transfer TR delivery of electricity certificates |

Transfer of tax liability regime - delivery of electricity certificates with a full right to deduct |

there must be document of self-assessment of VAT (for purchase) |

|

Application: |

It shall be used for the purchase of delivery of electricity certificates in Transfer of tax liability regime , it shall be stated on line 10/11 and 43/44 with full deduction. It shall be used for the sale of delivery of electricity certificates in Transfer of tax liability regime , it shall be stated on line 25 TR. |

|

9P |

Transfer TR delivery of electricity to the trader |

Transfer of tax liability regime - supply of electricity through systems or networks to the trader with a full right to deduct |

there must be document of self-assessment of VAT (for purchase) |

|

Application: |

It shall be used for the purchase in Transfer of tax liability regime , it shall be stated on line 10/11 and 43/44 with full deduction. It shall be used for the sale in Transfer of tax liability regime , it shall be stated on line 25 TR. |

|

AD |

Transfer TL gold with DE |

Transfer of tax liability regime - gold with shortened right to deduct |

There must be a self-assessment document |

|

Application: |

It shall be used for the purchase of gold in Transfer of tax liability regime , it shall be stated on lines 10/11 and 43/44 with DE. |

|

AND |

Transfer TL gold without D |

Transfer of tax liability regime - gold without right to deduct |

There must be a self-assessment document |

|

Application: |

It shall be used for the purchase of gold in Transfer of tax liability regime , it shall be stated on lines 10/11 TL. |

|

AU |

Transfer TL gold |

Transfer of tax liability regime - gold with full right to deduct |

There must be a self-assessment document (only for purchase) |

|

Application: |

It shall be used for the purchase of gold in Transfer of tax liability regime , it shall be stated on lines 10/11 and 43/44 in full. It shall be used for the sale in Transfer of tax liability regime , it shall be stated on lines 25 TR. |

|

AI |

Transfer TR investment gold brokerage |

Transfer of tax liability regime - intermediation in the delivery of investment gold with a full right to deduct |

there must be document of self-assessment of VAT (for purchase) |

|

Application: |

It shall be used for the purchase of provision of brokerage services in the supply of investment gold in Transfer of tax liability regime , it shall be stated on line 10/11 and 43/44 with full deduction. It shall be used for the sale of provision of brokerage services in the supply of investment gold in Transfer of tax liability regime , it shall be stated on line 25 TR. |

|

CK |

Provision of services by a foreign person with DE |

Provision of services by a foreign person with DE |

There must be a self-assessment document |

|

Application: |

It is used when providing a service by a foreign taxable necessary to reduce the right to deduct. It will be stated on lines 12/43 and 43/44 TR. |

|

CN |

Provision of services By foreign person without DE |

Provision of services by a foreign person without right to deduct |

There must be a self-assessment document |

|

Application: |

It will be indicated on line 12/13 TR. |

|

CS |

Provision of services By FP |

Provision of services by a foreign person |

There must be a self-assessment document |

|

Application: |

It is used when providing a service by a foreign taxable . It will be stated on lines 12/43 and 43/44 TR. |

|

CZ |

Sending articles from the EU to non-payers |

Sending articles from the EU to non-payers to non-payers |

|

|

Application: |

They will be used by persons registered for tax in another Member State when sending articles to the Czech Republic who are registered for tax in the Czech Republic (the place of supply is in the Czech Republic). It will be stated on lines line 1/2 TL. |

|

IWD |

Import of articles without DE |

Import of articles without right to deduct |

There must be a self-assessment document |

|

Application: |

Import of articles without right to deduct. It is included in line 7/8 DP. |

|

IWD |

Imp. Of art. adm. OT with DE |

Import of articles with DE |

|

|

Application: |

It will be stated on line 42 with DE. |

|

IE |

Imports of articles exempt |

Imports of articles exempt |

|

|

Application: |

It will be stated on lines 32 TR. |

|

IW |

Transfer TR import of articles originally warranty |

Transfer of tax liability regime - import of articles originally warranty |

there must be document of self-assessment of VAT (for purchase) |

|

Application: |

It shall be used for the purchase of articles provided as a guarantee in the implementation of this guarantee in Transfer of tax liability regime , it shall be stated on lines 10/11 and 43/44 with full deduction. It shall be used for the sale of articles provided as a guarantee in the implementation of this guarantee in Transfer of tax liability regime , it shall be stated on lines 25 TR. |

|

DA |

Transfer TR delivery of articles after assignment of retention of title |

Transfer of tax liability regime - delivery of articles after the transfer of the retention of title to the acquirer |

there must be document of self-assessment of VAT (for purchase) |

|

Application: |

It shall be used for the purchase of articles after the transfer of the retention of title to the acquirer, in Transfer of tax liability regime , it shall be stated on lines 10/11 and 43/44 with full deduction. It shall be used for the sale of articles after the transfer of the retention of title to the acquirer, in Transfer of tax liability regime , it shall be stated on lines 25 TR. |

|

DX |

Import of articles - CO |

Import of articles |

There must be a self-assessment document |

|

Application: |

It is used for the import of articles, where the tax administrator is the customs office on l. 7/8 and 42 TR. |

|

DY |

Import of articles with DE - CO |

Import of articles with DE |

There must be a self-assessment document |

|

Application: |

It is used for the import of articles, where the tax administrator is the customs office on l. 7/8 and 42 TR. |

|

DA |

When importing articles, the CO administration |

Import of articles |

|

|

Application: |

It will be stated on line 42 in full. |

|

E1 |

Aq. Asse. from EU with DE |

Acquisition of asset from EU with DE |

There must be a self-assessment document |

|

Application: |

It is used when acquiring asset from another EU state, when it is necessary to apply a reduction when entitled to a deduction. It is included in lines 3/4, 43/44 and l. 47 TR. |

|

E2 |

Aq. NMT from Non-payer from EU with DE |

Acquisition of MT from Non-payer from EU with DE |

There must be a self-assessment document |

|

Application: |

It is used when acquiring a new means of transport from another EU country from non-taxable persons, when a reduction must be applied to the right to deduct. It is included in lines 9 and 43/44 TR. |

|

E3 |

Acquisition and delivery of articles by an intermediary person |

Acquisition and delivery of articles by an intermediary person |

|

|

Application: |

It is used for the supply of articles within the EU in the form of triangular trade. It will be stated on line 30 when acquisition of articles of l. 30 when articles delivery. |

|

EA |

Aq. Asse. from EU |

Acquisition of asset from the EU |

There must be a self-assessment document |

|

Application: |

It is used when acquiring asset from other member state. It will be stated on line 3/4, 43/44 and l. 47 TR. |

|

EB |

Aq. NMT from Non-payer from the EU |

Acquisition of MT from Non-payer from the EU |

There must be a self-assessment document |

|

Application: |

It is used when acquiring a new means of transport from from persons not registered for tax in another Member State. It will be stated on line 9 and 43/44 TR. |

|

EK |

Aq. Asse. from EU with DE |

Acquisition of articles from EU with DE |

There must be a self-assessment document |

|

Application: |

It is used when acquiring asset from EU with reduced right to deduct tax, is included in line 3/4 and 43/44. |

|

EL |

Provision of services from EU with DE |

Provision of services from EU with DE |

There must be a self-assessment document |

|

Application: |

It is used when receiving service from EU with reduced right to deduct tax, is included in line 5/6 and 43/44. |

|

EM |

Aq. NMT from Non-payer from EU without DE |

Acquisition of MT from Non-payer from EU without reduction when to deduct |

There must be a self-assessment document |

|

Application: |

It is used when acquiring a new means of transport from from persons not registered for tax in another Member State without the right to deduct. It will be stated on line 9. |

|

EN |

Aq. Asse. from EU without DE |

Acquisition of articles from EU without reduction when to deduct |

There must be a self-assessment document |

|

Application: |

It will be stated on line 3/4 TL. |

|

ES |

Provision of services from the EU |

Provision of services from the EU |

There must be a self-assessment document |

|

Application: |

It is used when receiving service from another Member State from a registered payer. It will be stated on line 5/6 a 43/44 TL. |

|

EU |

Provision of services from EU without DE |

Provision of services from EU without reduction when to deduct |

There must be a self-assessment document |

|

Application: |

Used when receiving a service from the EU without the right to deduct. It will be stated on line 5/6 TL. |

|

EZ |

Aq. Asse. from EU |

Acquisition of articles from EU |

There must be a self-assessment document |

|

Application: |

It is used when acquiring asset from another Member State from a registered payer. It will be stated on line 3/4 a 43/44 TL. |

|

VNI |

Value of he transaction n. incl. in the coef. With DE |

The value of the transactions not included in the coefficient with the right to deduct |

|

|

Application: |

The value of the transactions not included in the coefficient with the right to deduct. Included in l. 51 with the right to deduct. |

|

ID |

Insolvency procedure with DE |

Insolvency procedure with DE |

|

|

Application: |

Debtor - reduced right to deduction, state on line 40/41 and 34 TR. |

|

IN |

Insolvency procedure |

Insolvency procedure |

|

|

Application: |

Creditor - to be indicated on line 1/2 and 33 TR. Debtor - full right to deduction, state on line 40/41 and 34 TR. |

|

ID |

Irrecovareble debt |

Irrecovareble debt |

|

|

Application: |

Creditor - to be indicated on line 1/2 and 33 TR. Debtor - full right to deduction, state on line 40/41 and 34 TR. |

|

IDD |

Irrecovareble debt with DE |

Irrecovareble debt with DE |

|

|

Application: |

Debtor - reduced right to deduction, state on line 40/41 and 34 TR. |

|

IG |

Investment gold |

Investment gold |

|

|

Application: |

Used to deliver exempt investment gold. It is included in line 26. |

|

CC |

Domestic charging of credit |

Domestic filling - charging of credit |

|

|

Application: |

Use in case of provided contribution in domestic land in case of charging electronic wallets, coupons e.t.c. It is included in. 1/2 DP. |

|

DC |

Domestic drawing of credit |

Domestic filling - drawing of credit |

|

|

Application: |

Use in case of provided contribution in domestic land in case of drawing electronic wallets, coupons e.t.c. It is included in. 1/2 DP. |

|

AS |

Domestic assets put into use |

Domestic assets put into use |

|

|

Application: |

Inclusion in the use of asset - full right to deduction, state on line 47 TR. |

|

AD |

Domestic assets put into use with DE |

Domestic assets put into use with DE |

|

|

Application: |

Inclusion in the use of asset - shortened right to deduction, state on line 47 TR. |

|

NI |

Not include to return |

Not include to return |

|

NII |

Not include to VAT, only Intrastat |

It is not included to return, it is included into Intrastat |

|

|

Application: |

Used when purchasing articles from a non-VAT payer from the EU. It can be used also on invoice out. It is not reported in the VAT return. |

|

NIR |

Not include to return - ratio without DE |

It is not included in return - ratio, the part without the right to deduct |

|

|

Application: |

It is used for the proportional part, which is not reported in the return (the payer is not entitled to a deduction) and belongs to the performance reported on line. 40/41 DP. |

|

WA |

Transfer TR waste |

Transfer of tax liability regime - waste |

there must be document of self-assessment of VAT (for purchase) |

|

Application: |

It shall be used for the purchase waste in Transfer of tax liability regime , it shall be stated on lines 10/11 and 43/44 in full. It shall be used for the sale of waste in Transfer of tax liability regime , it shall be stated on lines 25 TR. |

|

WD |

Transfer TL waste with DE |

Transfer of tax liability regime - waste with shortened right to deduct |

There must be a self-assessment document |

|

Application: |

It shall be used for the purchase waste in Transfer of tax liability regime , it shall be stated on lines 10/11 and 43/44 with DE. |

|

WWD |

Transfer TL waste without D |

Transfer of tax liability regime - waste without right to deduct |

There must be a self-assessment document |

|

Application: |

It will be used when purchasing articles according to Annex No. 5 to the Act in the regime of transfer of tax liability, it shall be stated on l. 10/11 TL. |

|

P2 |

Transfer TR delivery of gas to the trader |

Transfer of tax liability regime - supply of gas through systems or networks to the trader with a full right to deduct |

there must be document of self-assessment of VAT (for purchase) |

|

Application: |

It shall be used for the purchase in Transfer of tax liability regime , it shall be stated on line 10/11 and 43/44 with full deduction. It shall be used for the sale in Transfer of tax liability regime , it shall be stated on line 25 TR. |

|

P8 |

Surcharge for the sale of travel services in a special regime |

Surcharge for the sale of travel services in a special regime |

|

|

Application: |

It is used for Surcharge for the sale of travel services in a special regime. It will be stated on line 1/2 TL. |

|

P9 |

Surcharge for the sale of second - hand articles under a special scheme |

Surcharge for the sale of second - hand articles under a special scheme |

|

|

Application: |

It is used for Surcharge for the sale of second - hand articles under a special scheme. It will be stated on line 1/2 TL. |

|

EA |

Transfer TL allowances |

Transfer of tax liability regime - emission allowances |

there must be document of self-assessment of VAT (for purchase) |

|

Application: |

It shall be used for the purchase of emission allowances in Transfer of tax liability regime , it shall be stated on lines 10/11 and 43/44 in full. It shall be used for the sale of emission allowances in Transfer of tax liability regime , it shall be stated on lines 25 TR. |

|

AD |

Transfer TL allowances with DE |

Transfer of tax liability regime - emission allowances with shortened right to deduct |

There must be a self-assessment document |

|

Application: |

It shall be used for the purchase of emission allowances in Transfer of tax liability regime , it shall be stated on lines 10/11 and 43/44 with DE. |

|

RA |

Relocation of business assets to EU |

Relocation of business assets to EU |

|

|

Application: |

Relocation of business assets to other Member states in EU. Included in l. 20 TR. |

|

AWD |

Transfer TL allowances without D |

Transfer of tax liability regime - emission allowances without right to deduct |

There must be a self-assessment document |

|

Application: |

It shall be used for the purchase of emission allowances in Transfer of tax liability regime , it shall be stated on lines 10/11 TL. |

|

RAD |

Relocation of business assets to EU with D |

Relocation of business assets to EU with the right to deduct |

|

|

Application: |

Relocation of business assets to other Member states in EU with right to deduct. Included in l. 21 and l. 51 with the right to deduct. |

|

CP |

Transfer TL construction and assembly work included in the price of asset |

Transfer of tax liability regime - construction and assembly work included in the price of asset |

There must be a self-assessment document |

|

Application: |

It shall be used when purchasing services in the construction industry or for assembly work in the regime of transfer of tax liability included in the price of asset, it shall be stated on l. 10/11 and 43/ 44 a 47 in full. |

|

CD |

Transfer TL construction and assembly work included in the price of asset with DE |

Transfer of tax liability regime - construction and assembly work included in the price of asset with shortened right to deduct. |

There must be a self-assessment document |

|

Application: |

It shall be used when purchasing services in the construction industry or for assembly work in the regime of transfer of tax liability included in the price of asset, it shall be stated on l. 10/11 and 43/ 44 and l. 47 with DE. |

|

GR |

Group |

For compensation in group |

|

|

Application: |

Used by a member of the group or a representative member of the group, the tax does not apply to such compensation. It is not stated on any line of TL. |

|

CWD |

Transfer TL construction and assembly work without D |

Transfer of tax liability regime - construction and assembly work without right to deduct |

There must be a self-assessment document |

|

Application: |

It shall be used when purchasing services in the construction industry or for assembly work in the regime of transfer of tax liability, it shall be stated on l. 10/11 TL. |

|

SAW |

Transfer TL construction and assembly work |

Transfer of tax liability regime - construction and assembly work |

There must be a self-assessment document (only for purchase) |

|

Application: |

It shall be used when purchasing services in the construction industry or for assembly work in the regime of transfer of tax liability, it shall be stated on l. 10/11 and 43/44 in full. It shall be used when providing services in the construction industry or for assembly work in the regime of transfer of tax liability, it shall be stated on l. 25 TR. |

|

CW |

Transfer TL construction and assembly work - provision of workers |

Transfer of tax liability regime - providing workers for construction and assembly work |

There must be a self-assessment document VAT (only for purchase) |

|

Application: |

It shall be used when providing workers for construction and assembly work in the regime of transfer of tax liability, it shall be stated on l. 10/11 and 43/44 in full. It shall be used when providing workers for construction and assembly work in the regime of transfer of tax liability, it shall be stated on l. 25 TR. |

|

CWD |

Transfer TL construction and assembly work with DE |

Transfer of tax liability regime - construction and assembly work with shortened right to deduct |

There must be a self-assessment document |

|

Application: |

It shall be used when purchasing services in the construction industry or for assembly work in the regime of transfer of tax liability, it shall be stated on l. 10/11 and 43/44 with DE. |

|

D2 |

Domestic RC with DE, CR always B2 |

Domestic RC with deduction, CR always B2 |

|

|

Application: |

It will be used for received compensation in the Czech Republic with the obligation to reduce the right to deduct tax - repayment calendars if the amount of the repayment is up to CZK 10,000 and the amount of all repayment exceeds CZK 10,000. Domestic RC with It will be stated on line 40/41 TL. In the Control Report, it is always displayed in section B2, regardless of the amount of the repayment. |

|

DD |

Domestic RC with DE |

Domestic RC with DE |

|

|

Application: |

It will be used for received compensation in the Czech Republic with obligations to reduce the right to deduct tax and the remuneration provided for such compensation. It will be stated on line 40/41 TL. |

|

DWD |

Domestic |

Domestic compensations with Right to deduct |

|

|

Application: |

It also applies to compensation to non-payers of Member States, where Czech VAT is taxed. It will also be used when receiving payment. It will be stated on line 1/2 TL. It will be used for received compensation in the Czech Republic with full right to deduct tax and payments made for such compensations. It will be stated on line 40/41 TL. |

|

TP |

Domestic, CR always A4/ B2 |

Domestic compensations with Right to deduct, CR always A4/ B2 |

|

|

Application: |

It will be used for compensation in Czech republic - repayment calendars if the amount of the repayment is up to CZK 10,000 and the amount of all repayment exceeds CZK 10,000. Included for sale on line 1/2, purchase on line 1/2 40/41 DP. In the Control Report, it is always displayed in section A4,resp. in section B2 - regardless of the amount of the repayment. |

|

AD |

Tax deduction adjustment |

Tax deduction adjustment |

|

|

Application: |

The adjustment of the tax deduction is stated. It will be stated on line 60 TR. |

|

VA |

Delivery of a NMT to the payer EU |

Delivery of a new Means of Transport to the payer EU |

|

|

Application: |

It is stated for delivery of a new means of transport to other EU Member States to taxable persons . Included in l. 20 TR. |

|

VB |

Delivery of a new MT to non-payers in the EU |

Delivery of a new MT to the non-payer EU |

|

|

Application: |

It is stated for delivery of a new means of transport to other EU Member States to not . Included in l. 23 TR. |

|

VE |

Delivery of articles to EU |

Delivery of articles to EU |

|

|

Application: |

It is stated for the supply of articles to other EU Member States registered to taxpayers as an exempt compensation. Included in l. 20 TR. |

|

RT |

Tax refunded |

Tax refunded |

|

|

Application: |

It applies to tax refunds to individuals from third countries. It is included in line 61 TR. |

|

OE |

Other exports |

Other exports |

|

|

Application: |

It shall apply to other exempt compensation with the right to deduct and payments received. It is included in line 26. |

|

EA |

Articles export |

Articles export |

|

|

Application: |

It will be used for exports to third countries according to the SAD data. It will be stated on line 22. |

|

DC |

Deduction correction with DE |

Tax deduction correction with DE |

|

|

Application: |

The right to deduct when changing the regime, correcting the proportional coefficient, balancing the tax deduction with the reduced right to deduct on l. 45 TR. |

|

CD |

Deduction correction |

Tax deduction correction |

|

|

Application: |

The right to deduct when changing the regime, correcting the proportional coefficient, balancing the tax deduction with full the right to deduct and on line 45 TR. |

|

C. SECTION - value added tax |

|||||||||||||

I. Taxable compensation |

line |

Tax base |

Output tax |

||||||||||

Delivery of articles or provision of services with the place of compensation in the Czech Republic (eg § 13, § 14), distance selling of goods (§ 4 par. 9), distance sale of imported goods (§ 4 par. 10), delivery of goods facilitated by the operator of the electronic interface (according to § 13a), if in the case of these performances, the place of performance is in the Czech Republic and no tax has been declared through the special regime of one administrative place pursuant to Section 110a et seq. |

base |

1 |

TU,TV,52,55,CZ,P8,P9,KN,KP,IO |

IN |

|||||||||

reduced |

2 |

TU,TV,52,55,CZ,P8,P9,KN,KP,IO |

IN |

||||||||||

Acquisition of articles from other member state (§ 16, § 17 par. 6 letter e), § 19 par. 3) |

base |

3 |

EZ,EK,EN,EA,E1 |

|

|||||||||

reduced |

4 |

EZ,EK,EN,EA,E1 |

|

||||||||||

Acceptance of the service with the place of compensation according to § 9 par. 1 from a person registered to for tax in another Member State |

base |

5 |

ES,EL,EU,47,48 |

|

|||||||||

reduced |

6 |

ES,EL,EU,47,48 |

|

||||||||||

Import of articles (§ 23) |

base |

7 |

DB,DX,DY,01,02,43,45,49,4A |

|

|||||||||

reduced |

8 |

DB,DX,DY,01,02,43,45,49,4A |

|

||||||||||

Acquiring a new means of transport (§ 19 par. 4) |

9 |

EB,EM,E2 |

|

||||||||||

Regime of transfer of tax liability (§ 92a) - subscriber of articles or recipient of services |

base |

10 |

AU,AK,AN,AZ,DR,DV,OD,OK,ON,PE,PK,PN,SP,SQ,SR,SM,SC,SD,0P,0Q,0K,0L,0N,0O,0M,0R,0A,0B,21,2P,2K,2N,3P,3K,3N,4P,4K,4N,5P,5K,5N,6P,6K,6N,6M,6O,7P,7K,7N,8P,9P,P2 |

|

|||||||||

reduced |

11 |

AU,AK,AN,AZ,DR,DV,OD,OK,ON,PE,PK,PN,SP,SQ,SR,SM,SC,SD,0P,0Q,0K,0L,0N,0O,0M,0R,0A,0B,21,2P,2K,2N,3P,3K,3N,4P,4K,4N,5P,5K,5N,6P,6K,6N,6M,6O,7P,7K,7N,8P,9P,P2 |

|

||||||||||

Other taxable compensation for which he is obliged to declare the tax of the payer upon their receipt (§ 108) |

base |

12 |

CS,CK,CN,4B,4C |

|

|||||||||

reduced |

13 |

CS,CK,CN,4B,4C |

|

||||||||||

II. Other compensation and compensation with a place of compensation outside the country with the right to deduct tax |

Value |

||||||||||||

Delivery of articles to other member state (§ 64) |

20 |

VE,PM,VA,PO |

|||||||||||

Provide. services with the place of compensation in jčs defined in § 102 par. 1 let. d) and paragraph 2 |

21 |

50,5I,5Z |

|||||||||||

Export of articles (§ 66) |

22 |

AP |

|||||||||||

Delivery of a new means of transport to a person not registered for tax in jčs (§ 19 par. 4) |

23 |

VB |

|||||||||||

Selected performances (§ 110b par. 2) |

24 |

05 |

|||||||||||

Regime of transfer of tax liability (§ 92a) - supplier of articles or provider of services. |

25 |

AU,AZ,DR,DV,OD,PE,SP,SQ,0P,0Q,2P,3P,4P,5P,6P,7P,8P,9P,P2,21 |

|||||||||||

Other transactions with the right to deduct tax (eg § 24a, § 67, § 68, § 69, § 70, § 71h, § 89, § 90, § 92) |

26 |

IZ,VS,51 |

|||||||||||

III. Complementary data |

|||||||||||||

Simplified procedure for the delivery of article in the form of a tripartite trade (§ 17) by an intermediary

|

Acquisition of articles. |

30 |

E3 |

||||||||||

Delivery of articles |

31 |

E3 |

|||||||||||

Import of articles exempt pursuant to § 71g |

32 |

IE |

|||||||||||

Correction of the amount of tax on receivables from debtors in insolvency proceedings (§ 44) |

Creditor |

33 |

IN,IO |

||||||||||

Debtor |

34 |

IN,IK,IO,IP |

|||||||||||

IV. Right to deduct tax |

Tax base |

In full |

Shortened deduction |

||||||||||

From received taxable supplies from payers |

base |

40 |

|

TU,41,TV,4V,IN,IO |

TK,42,T2,4W,IK,IP |

||||||||

reduced |

41 |

|

TU,41,TV,4V,IN,IO |

TK,42,T2,4W,IK,IP |

|||||||||

When importing articles, where the tax administrator is the customs office |

42 |

|

DX,DZ,43,44 |

DY,DK,45,46 |

|||||||||

From taxable compensation reported on lines 3 to 13 |

base |

43 |

|

4B,49,47,ES,EZ,EB,01,03,EA,CS,AU,AZ,DR,DV,OD,PE,SP,SQ,SC,0P,0Q,0M,0R,21,2P,3P,4P,5P,6P,6M,7P,8P,9P,P2 |

EK,E2,02,04,E1, CK,EL,48,4A,4C, AK,OK,PK,SR,SD,0K,0L,0A,0B,2K,3K,4K,5K,6K,7K |

||||||||

reduced |

44 |

|

4B,49,47,ES,EZ,EB,01,03,EA,CS,AU,AZ,DR,DV,OD,PE,SP,SQ,SC,0P,0Q,0M,0R,21,2P,3P,4P,5P,6P,6M,7P,8P,9P,P2 |

EK,E2,02,04,E1, CK,EL,48,4A,4C, AK,OK,PK,SR,SD,0K,0L,0A,0B,2K,3K,4K,5K,6K,7K |

|||||||||

Correction of tax deductions according to § 75 par. 4, § 77, § 79 to § 79e

|

45 |

|

CD |

DC |

|||||||||

Total tax deduction (40 + 41 + 42 + 43 + 44 + 45) |

46 |

|

|

|

|||||||||

The value of the acquired property defined in § 4 par. 3 let. d) and e) |

47 |

|

41,4V,43,44,47,49, 4B,EA,MA,SC,0M,0R,6M |

42,4W,45,46,48,4A,4C,E1,MK,SD,0A,0B,6O |

|||||||||

V. Reduction of the right to deduct tax |

|||||||||||||

Exempt compensation without the right to deduct tax |

50 |

53.54 |

|

||||||||||

Value of compensation not included in the calculation of the coefficient (§ 76 par. 4)

|

51 |

With the right to deduct |

Without right to deduct |

||||||||||

52,55,PO,HN |

54 |

||||||||||||

Part of the tax deduction in the reduced amount |

52 |

Coefficient (%) |

|

Deduction |

|

||||||||

Settlement of tax deduction (§ 76 par. 7 to 10) |

53 |

Settlement coefficient (%) |

|

Change of deduction |

|

||||||||

VI. Calculation of tax liability |

|||||||||||||

Adjustment of tax deduction (§ 78 to § 78d) |

60 |

AD |

|||||||||||

Tax refund (§ 84) |

61 |

RT |

|||||||||||

Output tax (sum of 1 to 13 - 61 + tax according to § 108 not stated elsewhere) |

62 |

|

|||||||||||

Tax deduction (46 In full + 52 Deduction + 53 Change of deduction + 60) |

63 |

|

|||||||||||

Own tax liability (62 - 63) |

64 |

|

|||||||||||

Excessive deduction (63 - 62) |

65 |

|

|||||||||||

The difference compared to the last known tax when filing the additional tax. confession (63 - 62) |

66 |

|

|||||||||||

|

|

|

An overview of the types of taxes and their use in the One Stop Shop return from 1 July 2021

Abbr |

Description in K2 |

Detailed description |

||

OG |

OSS - EU scheme - article delivery |

Distance selling of goods to the final consumer in another EU country. |

||

OS |

OSS - EU scheme - provide service |

Provision of a service to the final consumer in another EU country. |

OI |

OSS - Import scheme |

Sales of imported article which are not subject to excise duty and whose own value of the consignment does not exceed EUR 150. This is a delivery of articles that is physically shipped or transported from a third country (eg USA, China) to the acquirer to an EU Member State by the supplier or on his behalf. |

OM |

OSS - Non EU scheme |

Provision of a service to a final consumer with a place of supply in the territory of the European Union by persons who do not have a registered office or establishment in the territory of the EU and do not apply this scheme in another Member State. |

The relevant type of tax also applies to advances that precede performance (applies to all 3 schemes).

|

|

|

Standard date for VAT

For the purposes of further interpretation of the issue in this chapter, the term Standard Date for VAT will be understood as the date according to which a decision is made as to whether or not a certain document falls within the specified period

IO, II, AI, AO is standard date the Tax point date in the header of the document, which is the date of the taxable supply in terms of VAT. If the Invoice Date is zero, the document does not enter into the VAT return.

For IN, PO and BS, the authoritative date is the Invoice date on the item of the document, which is the date of the taxable compensation from terms of VAT. If the Invoice Date is zero on document item, the document does not enter into the VAT return.

Date of the accounting transation and standard date for VAT in different periods:

Sometimes there may be a situation where the Date of the accounting transaction and the Invoice Date on one document fall into another tax period. In such a case, it is appropriate to repost the amounts from individual VAT analysts to the auxiliary analytical account for VAT on the last day of the tax period with a general accounting document. The amounts are recalculated on the first day of the following tax period. Process is described in chap. Checking VAT account balances.

|

|

|

Documents with VAT and documents without VAT

Even if the document has a standard date for VAT falling within the selected period and is included for processing, it may not always be taken into account when calculating VAT. It also depends on whether it is “Document with VAT or documents without VAT”.

- For IO and II, on the Basic data tab in the tax recapitulation, there is a VAT flag, which determines whether the given item of the document is considered as a “document with VAT" (checked) or as a "document without VAT" (unchecked).

- For AP and AR, the status of the document item is a Tax Document, which determines whether the advance item is considered a "document with VAT" (the advance item is in the Tax Document status) or as a "document without VAT" (the item is not in the Tax Document status).

- For OR and OL, there is a VAT flag in the header, which determines whether the items of the document are considered as "document with VAT" (checked) or as a "document without VAT" (unchecked)

- For IN, PO and BS, there is a VAT flag on item, which determines whether the items of the document are considered as "document with VAT" (checked) or as a "document without VAT" (unchecked).

The following rules apply:

- Items of “documents with VAT” are always taken into account when calculating VAT. Exceptions are tax types listed in the calculation parameter Tax types not included in the calculation (e. g. tax type "N").

- “Documents without VAT "are not taken into account when calculating VAT. Exceptions are tax types listed in the calculation parameter Tax types included in the calculation even without VAT check (e. g. tax types VE, PM, 50, ...). In the event that IO and II are to enter the VAT return and the provided (received) advance for these invoices is not to enter, the given advance tax type "N" - Do not include in the return, zero tax rate, is not a tax document and has not checked the VAT flag.

|

|

|

Methodologies for VAT, import and export

|

|

|

Taxation of acquired articles from the EU

Taxation of acquired articles (services,..) from another Member State from a person who is registered for VAT in another Member State.

Whereas the supply of articles (services,…) between VAT payers within the EU, it is considered an exempt taxable compensation with the right to deduct VAT, the purchaser of articles (Czech VAT payer) will buy articles at a price without tax. They are obliged to declare and tax the acquired goods in the Czech Republic as part of their VAT return (applying the rates of the Czech Republic according to the VAT Act) and, if they have a proper tax document, they will apply a deduction.

In this business case, one invoice received includes two courses - one from the day when the invoice is received by the customer (this course is a course for accounting), and the other from the day when the supplier issued the document (this course is a course for VAT).

In connection with this topic was in K2 IS created a function which, after the introduction and confirmation of an invoice in in IS K2, automatically creates an internal document (hereinafter this document is referred to as "self-assessment document”), on which VAT is calculated. This self-assessment document is used both to post VAT and to enter into the calculation of the VAT return.

Before we start using the function, it is necessary to set parameters for creating self-assessment documents, see chap. Settings for creating self-assessment documents.

|

|

|

We enter the received invoice into the system in the usual way, at the accounting rate, we guide the invoice items with the correct VAT rate according to the VAT Act, but we do not check the VAT flag on the Basic data tab.

On the Basic data of the document tab, we also select the correct type of tax. For example: "EZ" for received compensations with the right to deduct VAT according to §72, "EK" for a reduced claim, "EN" for received compensation for which the payer is not entitled to deduct tax according to §75 of Act no. on VAT, or another appropriate type of tax.

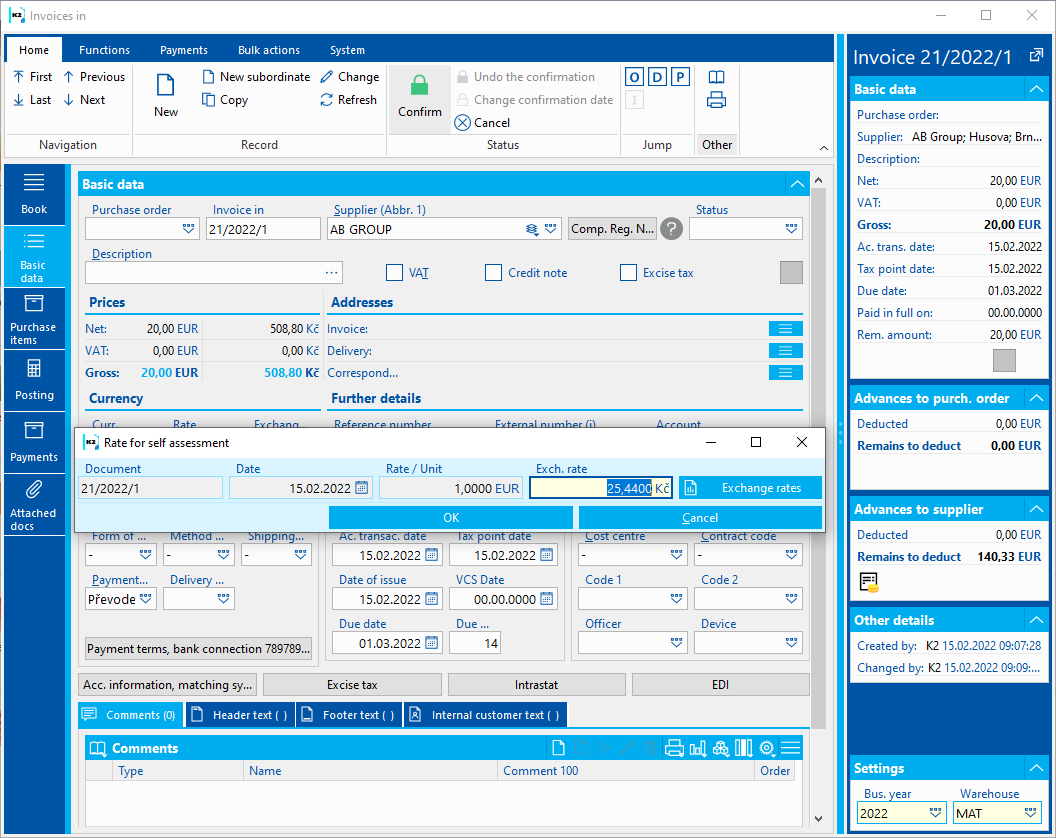

We will save and confirm the document. When confirming the invoice, a form will appear asking for the invoice date and the rate of the self-assessment document. After approving this data, an internal document is automatically created in the book intended for self-assessment documents.

The creation of tax invoices when confirming an invoice received is performed when the tax type has the VAT self-assessment flag checked.

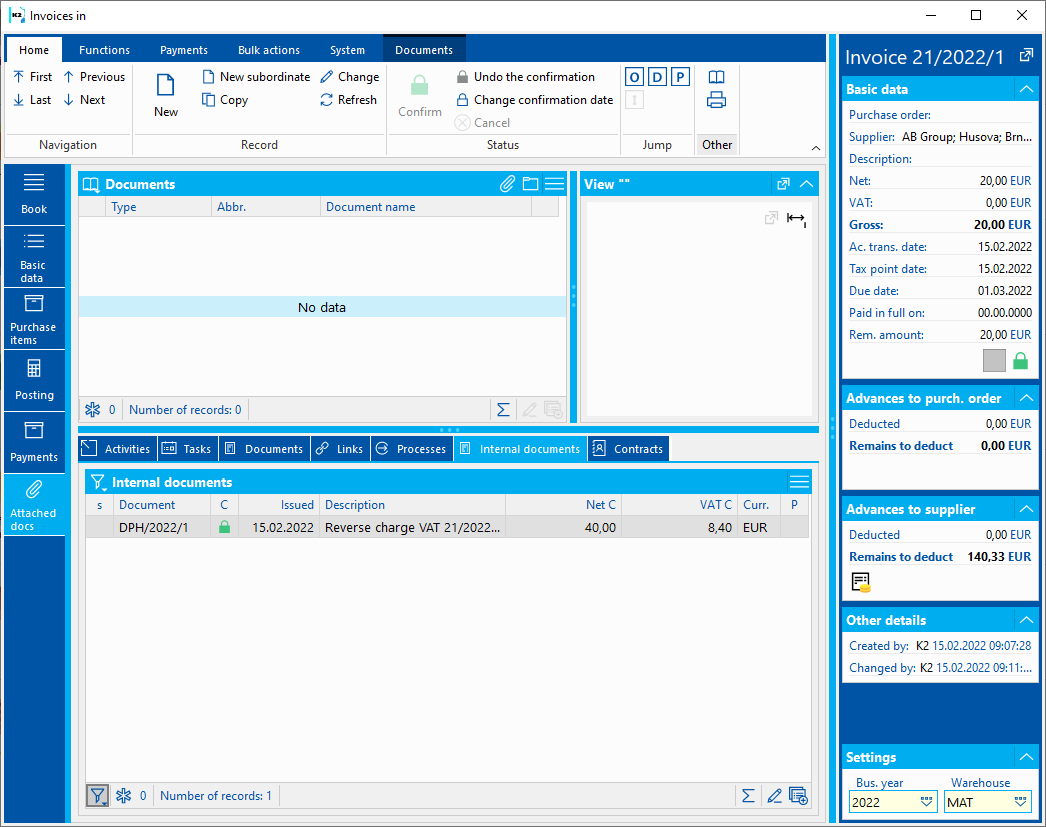

The invoice and internal document are automatically linked:

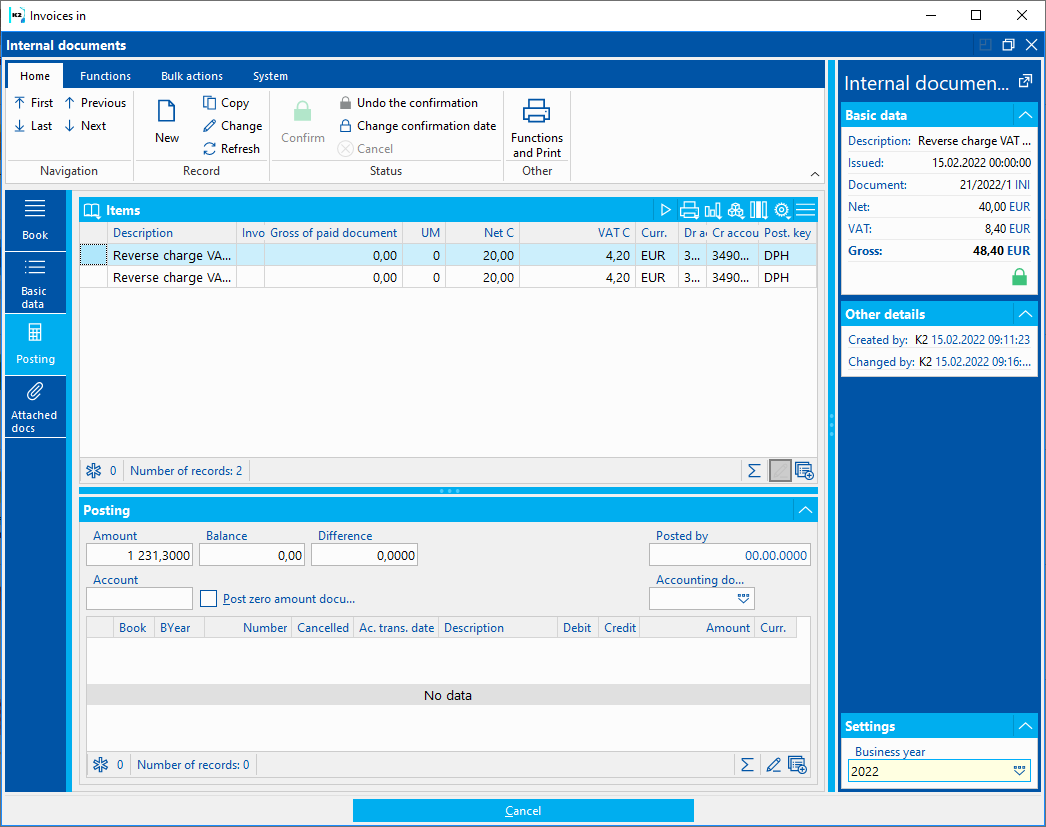

- in the header of the internal document, the received invoice is saved in the Document field;

- on the Attachments tab, the Internal Documents tab displays a link to the internal document.

If the invoice changes the type of tax to the type of tax for which the self-assessment document is not issued, then when you try to confirm the changed invoice, you will be asked: "There is an not canceled self-assessment document for this invoice. Do you want to cancel it?"

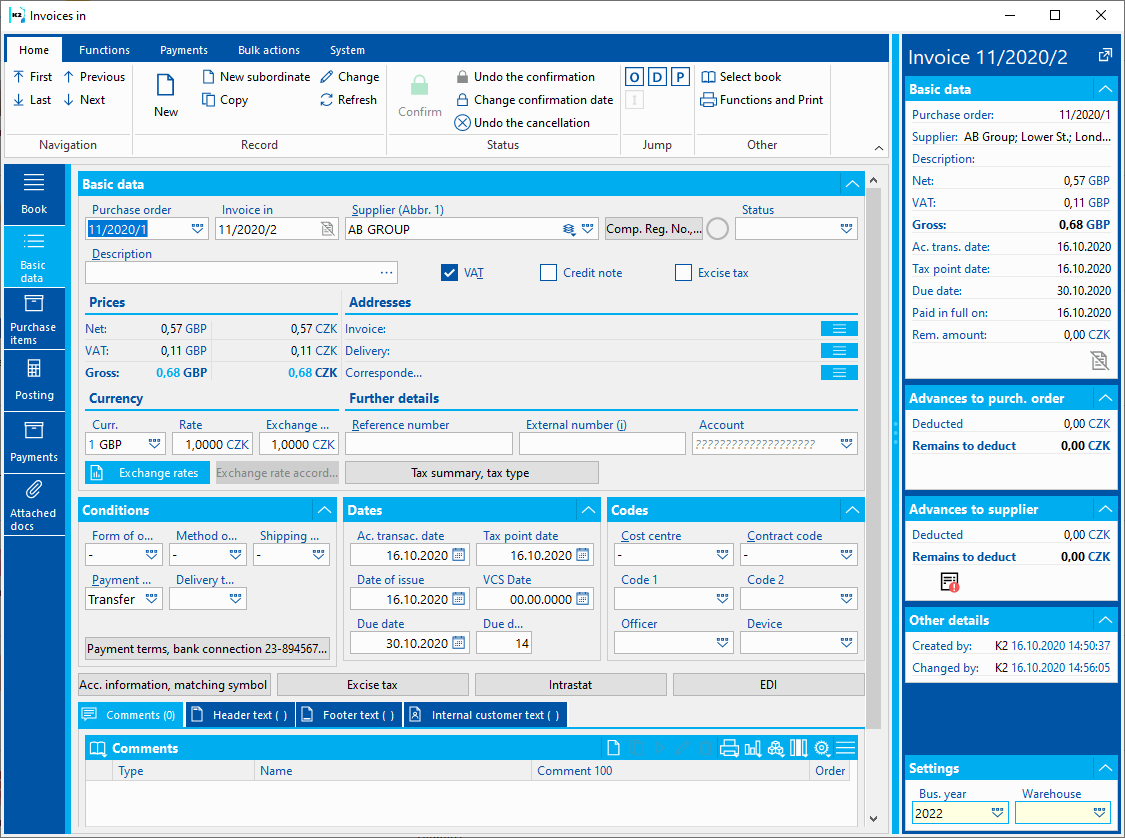

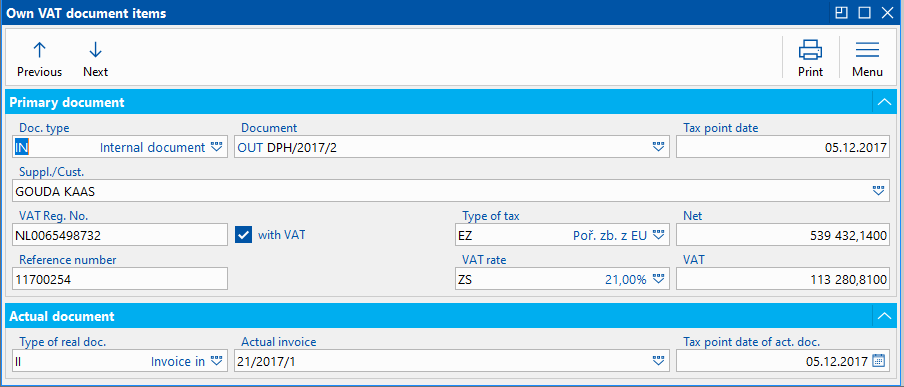

Picture: Invoice In - Basic Data tab

Picture: Invoice In - Basic data tab - when confirming the document, a query for the invoice date and the rate of the self-assessment document will appear

Picture: Invoice In - Attachments tab, Internal documents

Invoices received are charged in the usual way. Here is an example of accounting if the tax type is "EZ", "EK" or "EN".

Debit side account |

Credit side account |

Amount |

111 |

321 |

Net |

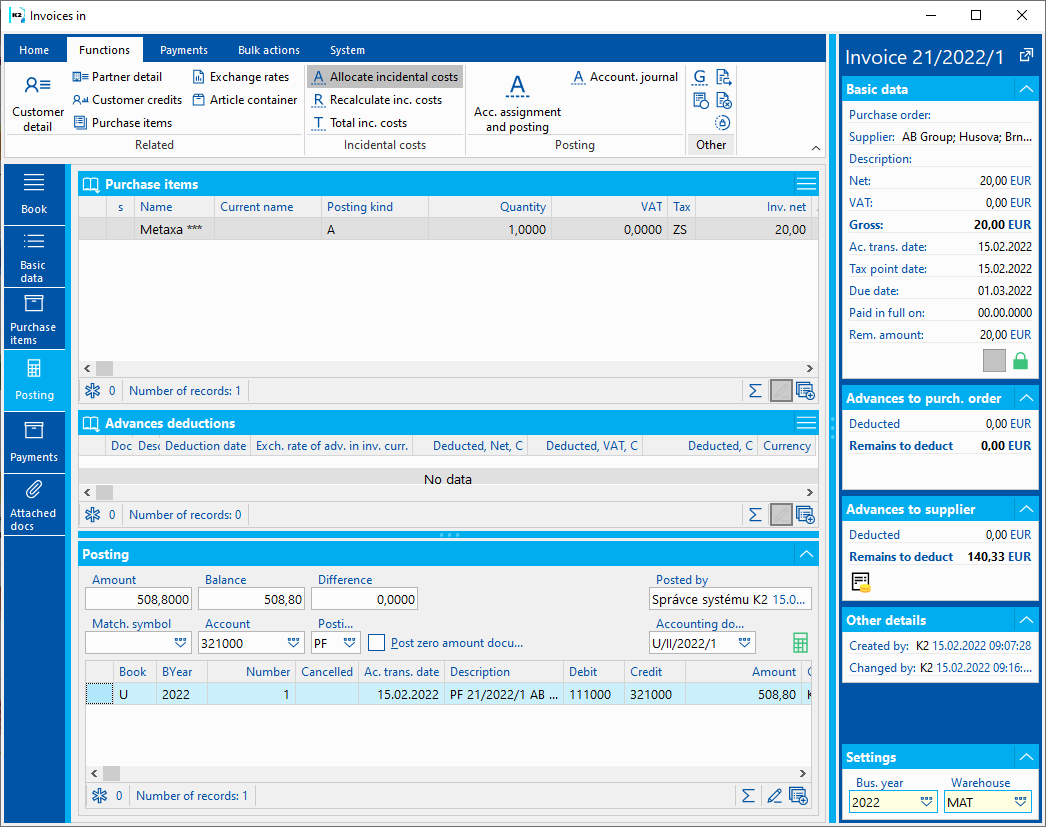

Picture: Invoices in - Posting tab

|

|

|

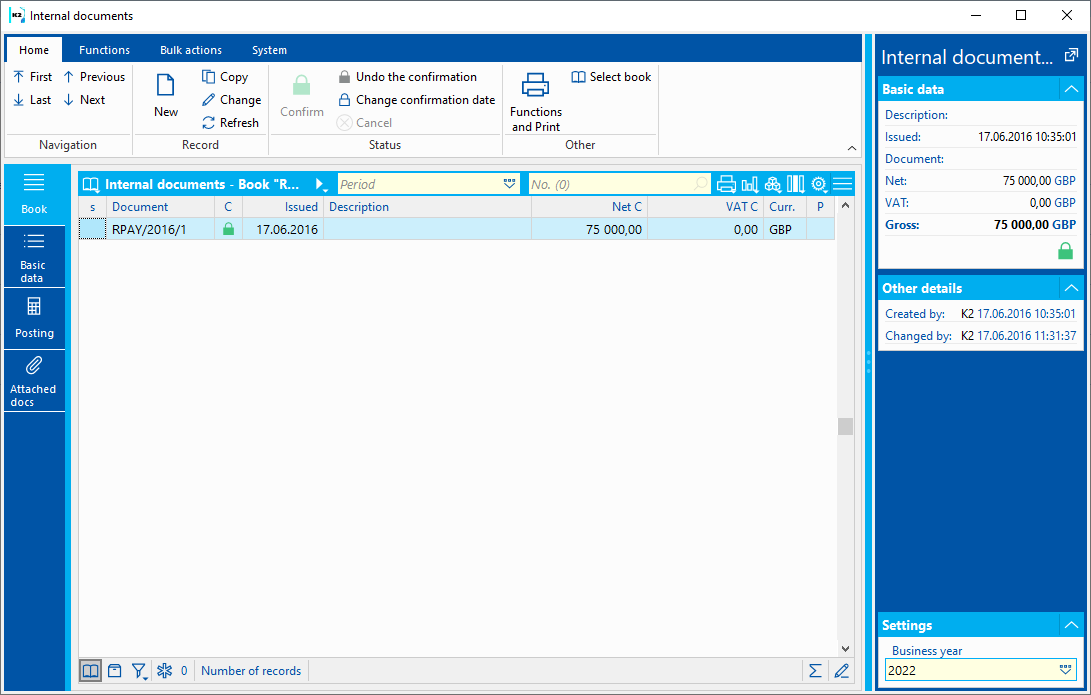

An internal document is automatically created when the invoice received is confirmed. In the header, in the Document field, there is a link to the invoice. If the self-assessment of VAT is applied on input and output, there are 2 items on the internal document (item for application on input and item for application on output), the VAT flag is checked on the items.

Picture: Internal document - Basic Data tab - VAT selfass.

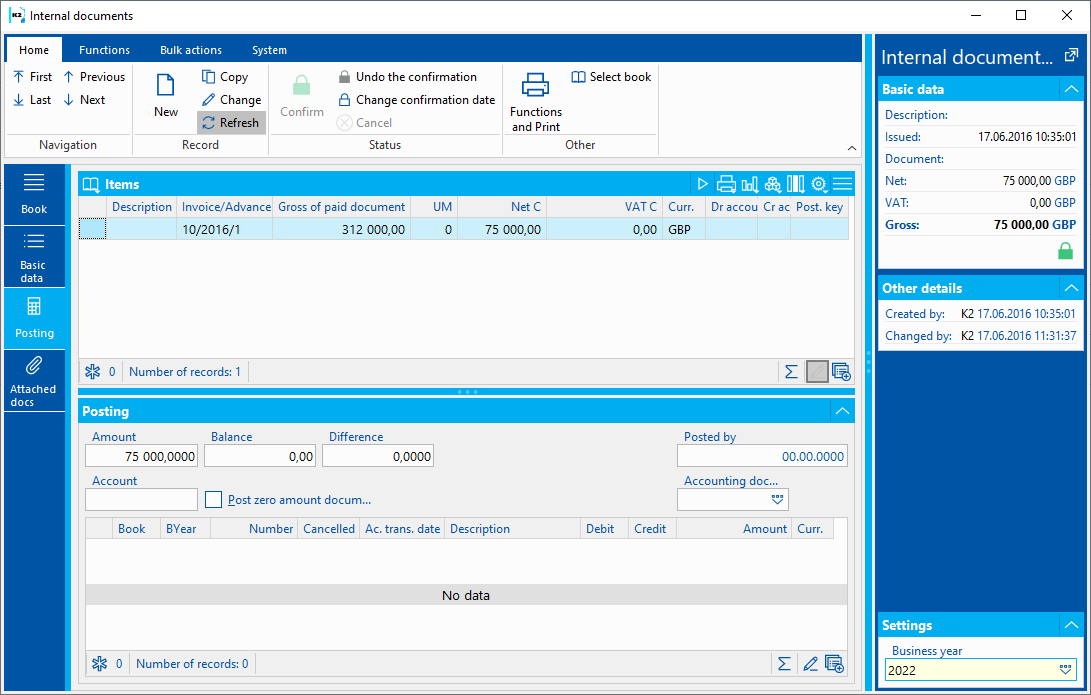

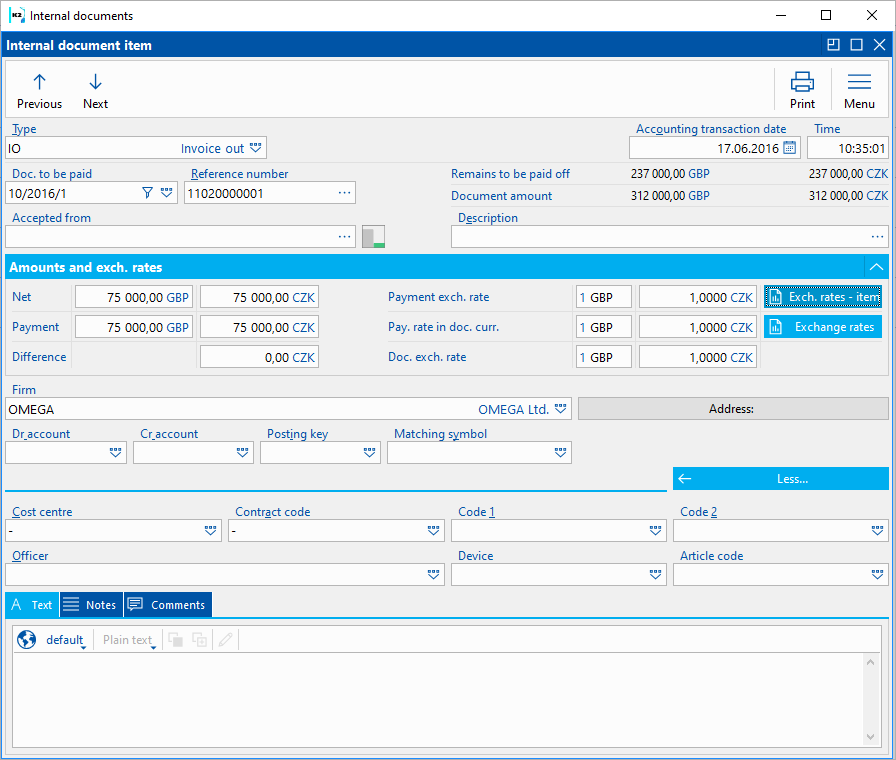

Internal document items copy the invoice tax recapitulation items - each internal document item has the same net amount, VAT rate, type of tax.

Picture: Internal document - Posting tab - Items - VAT selfass.

Picture: Internal Document item - self-assessment of VAT

We post internal documents as follows:

Tax type "EZ" or "EK" (VAT is reported on input and output):

Item Type |

Debit side account |

Credit side account |

Amount |

Output |

349 - VAT equalization account |

343 - VAT on output |

VAT |

Input |

343 - VAT on Input |

349 - VAT equalization account |

VAT |

The VAT balancing account is substituted for the internal document item from the Debit side account and Credit side account settings in the Internal Documents Book.

Tax type "EN" (VAT is reported only on output):

Item Type |

Debit side account |

Credit side account |

Amount |

Output |

111 - acquisition of articles |

343 - VAT on output |

VAT |

If VAT is reported only on output, the acquisition account is substituted for the item of the internal document from the Parameters of self-assessment documents - parameter Balancing account of VAT self-assessment only on output.

Accounting for other types of taxes is similar.

Picture: Internal document - Posting tab - VAT self-assessment posting

|

|

|

New document with type of tax, which has the Self-assessment of VAT checked (e. g. EZ, EK, EN, ...), the form VAT return: C. SECTION - value added tax according to following rules:

- For types of taxes where VAT is paid only on output, the classification is determined only by whether the invoice date of the internal document is from the reported period.

- The following rules apply to types of taxes where there is input and output tax:

- If the invoice and the internal document have the invoice date in the reported period, the input and output tax will appear.

- If the invoice has an invoice date from a different period than the internal document, then if we report VAT for the period to which the internal document belongs, output tax will appear. If we report tax for the period to which the invoice falls, input tax will appear.

- In the case of a separate internal document that has an invoice date in the reporting period, the output tax will appear.

- In the case of a separate invoice, nothing happens, such an invoice lacks a document on which the VAT is calculated. This is a error variant.

- In the case of a pair of advance and internal document, the input and output tax will always appear according to the period of the internal document.

|

|

|

Module VAT settings

|

|

|

Code list.

|

|

|

Type of return of Tax with value added. It is inserted into the VAT document automatically according to the selected calculation.

Picture: Type of tax return code list

|

|

|

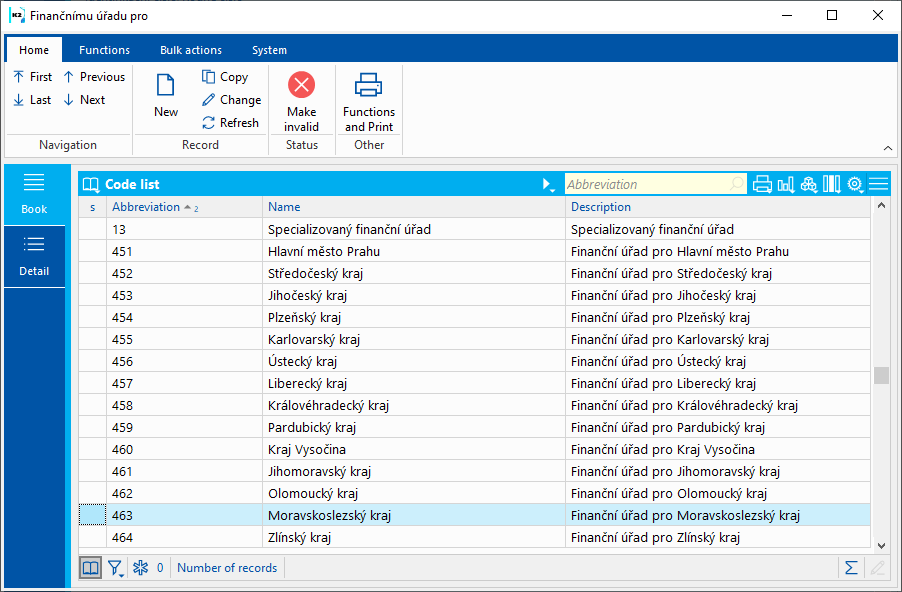

List of tax offices for

Picture: Tax office for code list

Description of Fields:

Abbr |

Tax office code |

Name |

Tax office name |

Description |

Tax office description |

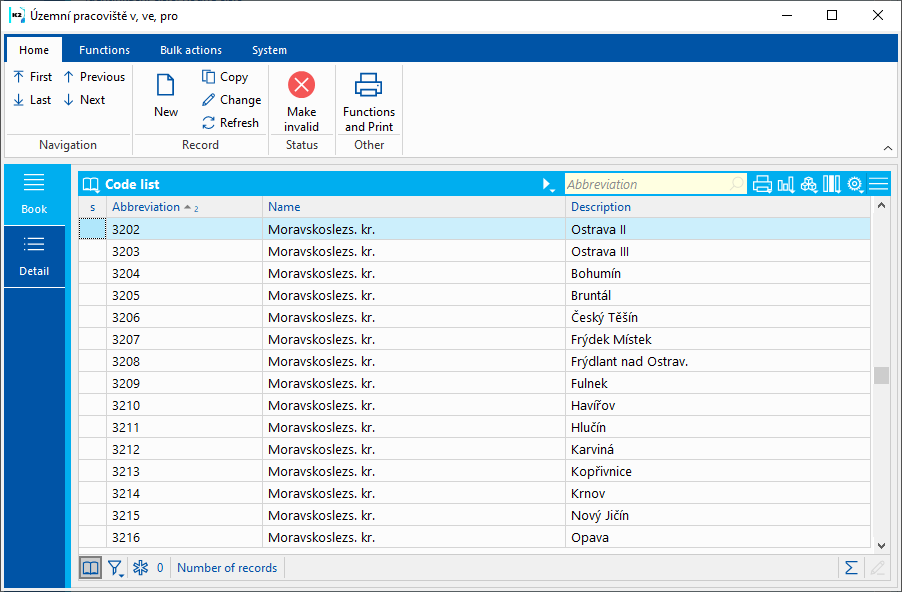

List of territorial workplaces in

Picture: Code list List of territorial workplaces in

Description of Fields:

Abbr |

Territorial workplace code |

Name |

Territorial workplace name |

Description |

Territorial workplace description |

|

|

|

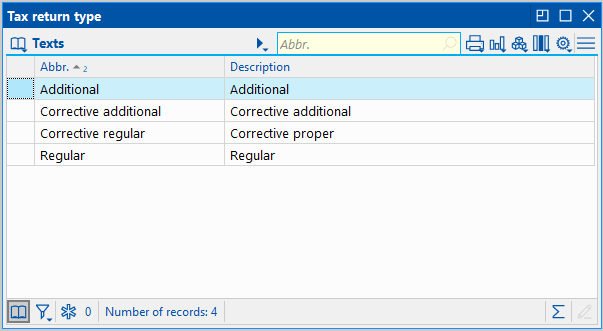

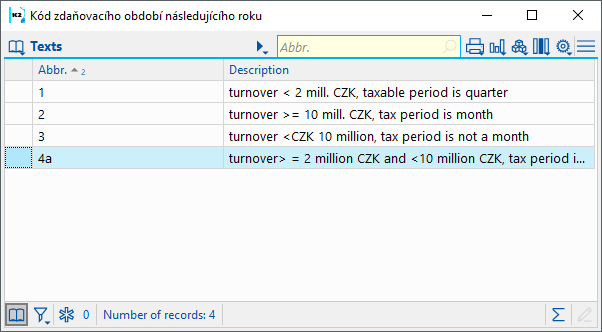

It is filled in in the proper return for the last tax period of the calendar year.

Picture: Code of the tax period of the following year code list

Description of Fields:

Abbr |

Code of tax period |

Description |

Description. |

|

|

|

Representative type code

Picture: Code list Representative code

Description of Fields:

Abbr |

Representative code |

Description |

Description. |

|

|

|

Settings for creating self-assessment documents

Self-assessment documents are created when we purchase articles / services without VAT, and then tax them as part of our VAT return (input, output). It is used, for example, when acquiring articles and services from the EU or when purchasing in the regime of transfer of tax liability.

Upon confirmation of the invoice received, other liability, or cash or internal document with the appropriate type of tax, a self-assessment document (internal document) is automatically created in IS K2, on which the VAT is calculated. Thist document is used both to post VAT and to enter into the calculation of the VAT return.

The following chapters describe the settings of the book of internal documents in which the self-assessment documents are created and the settings of the parameters for the creation of self-assessment documents.

|

|

|

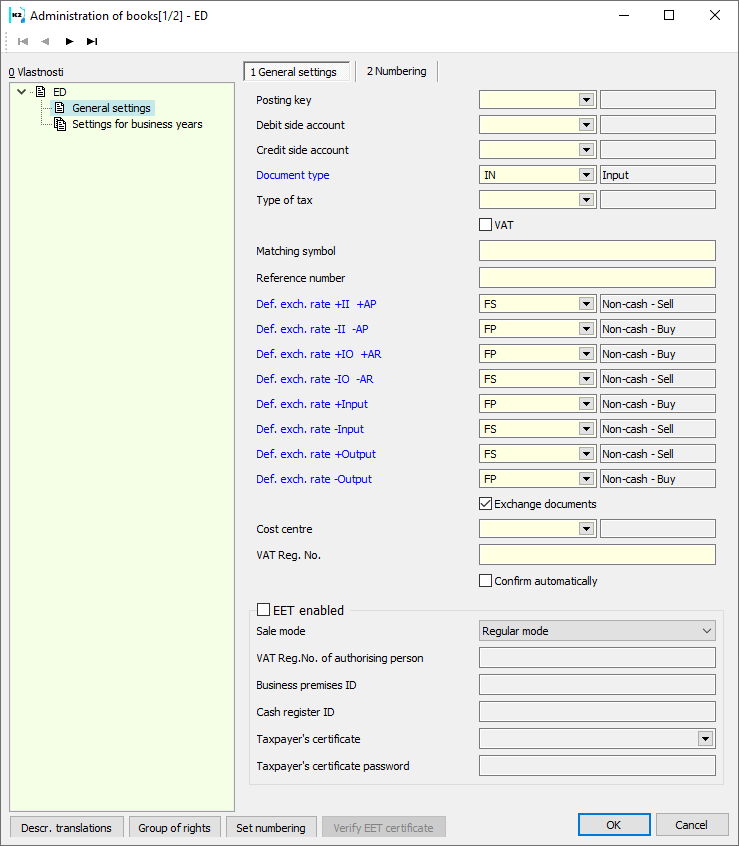

We will create a book of internal documents, in which self-assessment documents will be created.

Picture: Internal Document books setting - self-assessment of VAT

Description of selected fields:

Posting key |

Posting key for posting VAT self-assessment (only VAT posting is set in the posting key). |

Debit Side Account |

VAT balancing account - e. g. "349000". |

Credit Side Account |

VAT balancing account - e. g. "349000". |

Document type |

We set “OU” - Output |

|

|

|

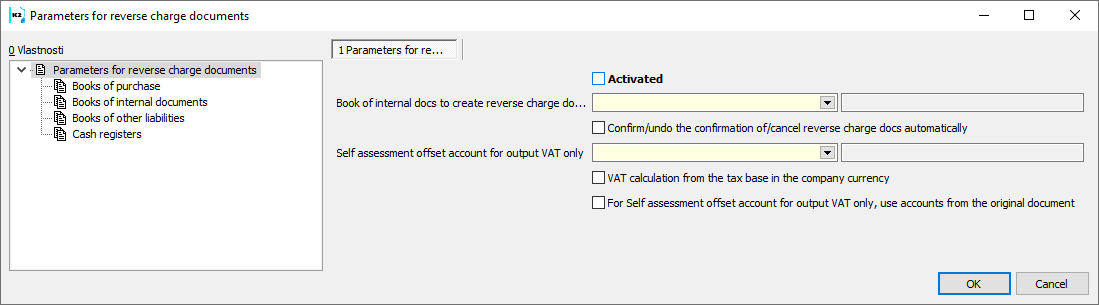

We set the parameters by running the function Parameters of self-measurement documents from the tree menu Accounting - VAT - Basic settings.

Picture: Parameters of self-measurement documents form

Activate the function by checking the On box.

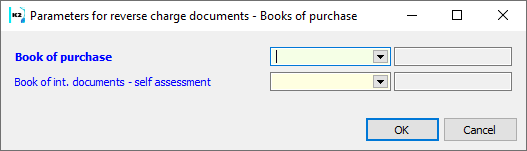

If we record self-assessment documents in one book, we set the following parameters:

Book of internal documents for creating self-assessment documents |

A book in which only self-assessment documents will be created. |

Balancing account of self-assessment of VAT only on output |

An account to be added to the self-assessment document if VAT is reported only on output. |

Automatically unconfirm / confirm / cancel selfass. documents |

Checking the box will be performed upon confirmation of the invoice received, other liability, or cash receipt or internal document, automatic confirmation of the self-assessment document. Checking the box will be performed upon undo the confirmation of the invoice received, other liability, or cash receipt or internal document, automatic confirmation of the self-assessment document. If the field is unchecked, a query will be displayed when the document is confirmed: "There is confirmed self-assessment document for this document. Do you want to undo the confirmation?" Checking the box will be performed upon cancelation of the invoice received, other liability, or cash receipt or internal document, automatic confirmation of the self-assessment document. If the field is unchecked, a query will be displayed when the document is canceled: "There is not canceled self-assessment document for this document. Do you want to cancel it?" |

Calculation of VAT from the tax base in the company currency |

The option affects the calculation of the amount of VAT in the company currency on the self-assessment document: - Off: VAT=VAT in the currency of document * Rate |

Use the accounts from the original document for the VAT self-assessment balancing account only at the output. |